WePay — Keap's embedded payment processor — was acquired by Chase and shut down for third-party integrations. Thousands of active merchants suddenly couldn't collect payments. I had five months to build a replacement from scratch, migrate 70% of affected customers, and ship it without breaking anyone's existing business.

RoleSole Product Designer

TimelineOct 2023 – Feb 2024

Duration5 Months

TeamProduct, Engineering, Payments

$70M+

Transactions processed via new system

73.9

SUS score — above industry average

+30%

Payment volume increase post-launch

70%

WePay customers migrated on time

Sections

01

The trigger — WePay shutdown, five months to replace it

WePay

a Chase company

Deprecated

Platform no longer supported

3rd-party access ended

External integrations discontinued

Acquisition → Shutdown

5-month deadline to replace

70%

70% of merchantsmigrated on time

Keap Pay

Integrated · Keap-owned

KYC onboarding

Streamlined verification

Payouts

Faster, more reliable

Recurring billing

Built-in subscription management

Oct 2023Migration period begins

5-month deadlineReplace WePay

Feb 2024Migration period ends

WePay (acquired by Chase, third-party integrations shut down) → 5-month sprint → Keap Pay, integrated and Keap-owned. 70% of WePay customers migrated on time. KYC-compliant onboarding, payout dashboard, and recurring billing built from scratch.

Small business owners rely on Keap to collect payments. When WePay was acquired and shut down for third-party integrations, thousands of active merchants faced immediate disruption — invoices they'd already sent couldn't be paid, recurring billing stopped working, and there was no fallback. With competitors launching embedded payments, we had one chance to replace WePay with something better.

The Real Problem

It wasn't just a migration. WePay's shutdown exposed how fragile a third-party processor dependency is. The real mandate was to build an embedded, Keap-owned payments product — not just swap one vendor for another.

My Role

Sole designer. End-to-end UX responsibility: onboarding, payment processing, migration flow, dashboards, and every customer-facing touchpoint. No existing payment component library to build on.

5-month hard deadline

Tied to the WePay shutdown date. Every week of slip meant more merchants without a way to collect payments.

Legal compliance

KYC and PCI-DSS requirements built into every form step. Not optional, not deferrable.

Migration constraint

Could not disrupt active merchants mid-transaction. Every existing payment link, invoice, and subscription had to keep working during the transition.

Engineering constraint

The engineering team was learning the new payment provider's API (Rainforest) in parallel with my design. Design and implementation had to move at the same pace.

Competitive analysis — Keap Pay benchmarked against Stripe, Auth.net, EVO, eWay, and PayPal across transaction fees, card types, compliance, recurring billing, ACH, and key differentiators. Keap Pay's built-in Hosted Service and Payments Concierge were unique advantages.

Design Studio: Keap Pay — cross-functional workshop with product, engineering, and payments teams to align on what "good" looks like before writing a single spec. Covered onboarding questions, user flow sketches, and iteration synthesis.

Migration flow — two user paths: existing WePay users migrating to Keap Pay, and users coming from other processors. Both needed to complete the same onboarding and reach the same active state.

Before touching a screen, I ran five discovery interviews with SMB owners currently using WePay — supplemented by competitive analysis across the four processors we were benchmarking against. The goal was to understand the mental models and frustrations of non-technical business owners handling payments, not just the feature checklist.

"I don't know if I set this up right. I just want to know when the money hits my account."

— SMB Owner, Service Business

"The old system asked for so much information and never told me if I was approved. I got anxious every time."

— SMB Owner, Retail

"I'm not a tech person. If there's a payment issue, I need to know fast and know what to do about it."

— SMB Owner, Health & Wellness

P1

Build trust first

Merchants are handing over sensitive financial information. Every screen must signal security, legitimacy, and forward progress clearly — not just legally comply with it.

P2

Reduce cognitive load

Break multi-step forms into digestible chunks with clear progress indicators. Never show a wall of fields. KYC is necessarily complex — the design's job is to hide that complexity from the user.

P3

Transparent payout timeline

Show merchants exactly when they'll get paid. Uncertainty breeds distrust — clarity builds loyalty. This was the most common frustration with WePay and the easiest win to design for.

03

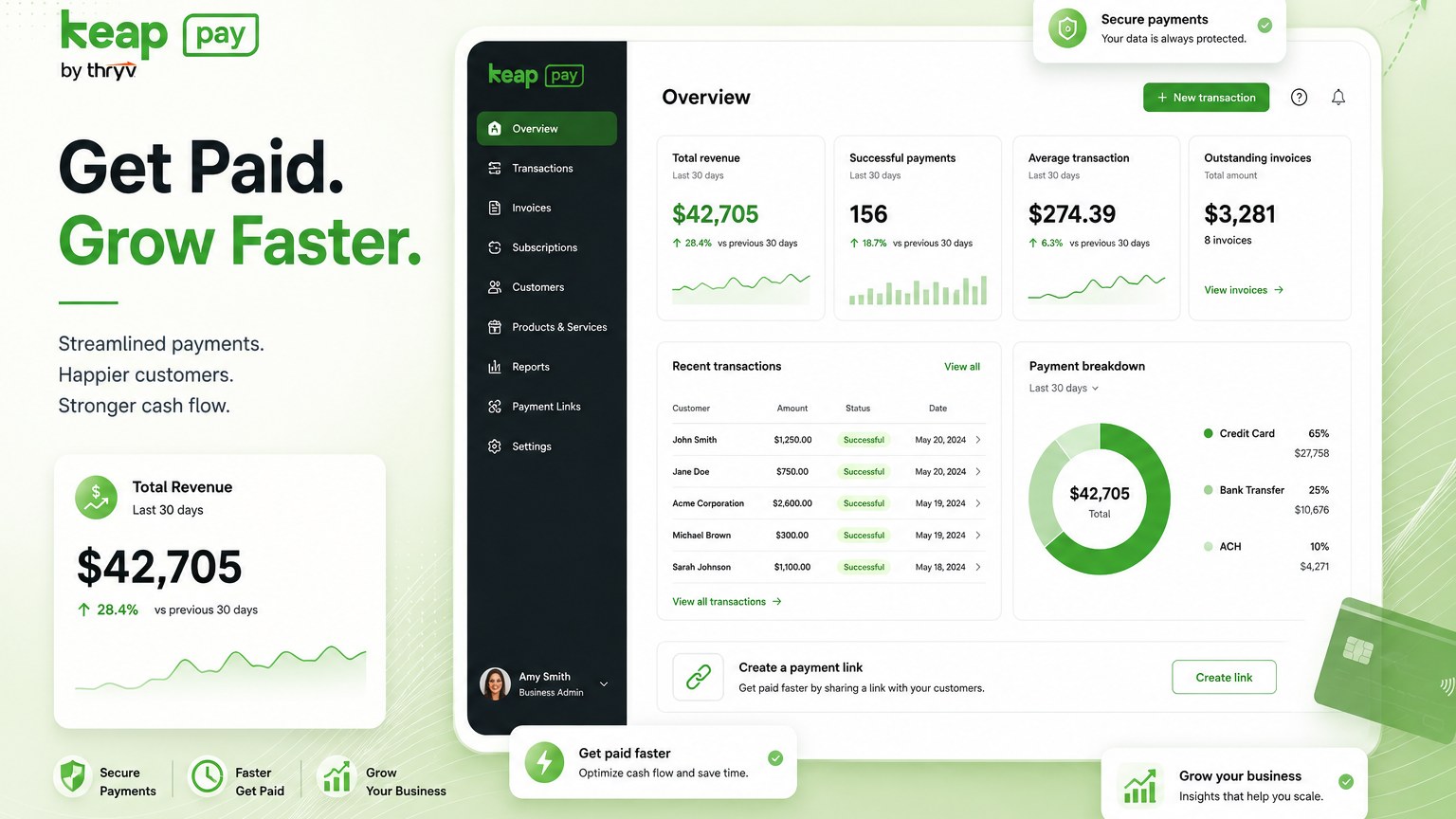

Design — from blank canvas to end-to-end payments product

Rainforest API integration — built custom UI components on top of Rainforest's hosted form SDK. Credit card and bank transfer tabs, hosted form with validation, payment report dashboard. All built alongside engineering learning the API in real time.

03a

Custom component library — built from scratch

Payment component library built from scratch — status bar, hosted payment forms (credit card + bank transfer), pagination, tabs, stacked inputs, review table. No existing Keap design system covered payment-specific UI patterns, so every component was designed and documented new.

03b

Prototype walkthrough — the flows in motion

▶ Prototype walkthroughsClick to play each flow

Prototype walkthroughs — the 6-step onboarding flow, the payment dashboard, and the sign-up page draft. The final sign-up page (iterated after usability testing) follows section 04.

03c

Payment page — before vs. after

Before — WePay / third-party processors

+

Search

Home

Contacts

My day

25Comms

Sales

Marketing

Automation

Reports

9+

← Payment processing and currency

Currency settings

This is the currency the application will use for all billing, payments and invoices.

CurrencyUS Dollar [USD]

▾

Payment processing

Manage how you collect payments from your clients. All Keap accounts are enrolled to accept payments.

wepayA CHASE COMPANY

WePay

Accept Visa, Mastercard, American Express and Discover. 2.9% flat rate + .30 cents transaction, no hidden fees.

Default account

Email

muzzylmz@gmail.com

Account Status

Pending

Manage ▾

stripe

Stripe

2.9% flat rate + 30 cents transaction, no hidden fees.

Before (WePay): a third-party processor list with no ownership and generic "Connect" CTAs. After (Keap Pay): a Keap-owned experience with Keap Pay featured prominently and clear value props.

01

Show business name, not just amount

Customers paying an invoice want to see who they're paying. Displaying the business name prominently builds trust and reduces disputes — a small change with measurable impact on completion rates.

02

Inline security cues at the moment of anxiety

Security signals placed near the card field — not buried in footers. Users feel most anxious when entering card details; that's exactly where trust signals need to appear, not below the fold.

03

Dedicated payout dashboard

Built a dedicated payouts timeline view so merchants always know exactly when to expect funds. This eliminated the #1 support inquiry ("Where's my money?") and turned a frustration point into a feature differentiator vs. WePay.

04

Testing — validated throughout, not just at the end

I ran moderated task-based usability sessions throughout the design process — not just at the end. This meant catching issues early and iterating before engineering built the final version. Sessions were recorded and analyzed for hesitation points, errors, and moments of confusion — not just task completion rates.

73.9

SUS Score

"Good" benchmark — above industry average for payment products, which typically score 65–70

40%

Faster signup

After removing redundant KYC fields and consolidating steps based on testing findings

95%

Self-serve setup

Users completed full payment setup without contacting support post-launch

F1

Simplified signup reduced friction

Users completed onboarding 40% faster after we removed redundant fields and consolidated the KYC steps into a clearer sequence. The original form had asked for the same information in two different steps.

F2

Migration path reduced user anxiety

Transparent communication about exactly what would and wouldn't transfer from WePay significantly reduced anxiety in testing sessions — and cut support tickets post-launch.

F3

Dashboard improved payment visibility

Users appreciated the consolidated view of payments and payouts. Several said this was "the one thing WePay never had." One user: "I can actually see when my money is coming. That alone makes it worth switching."

F4 →

Sign-up page had too much text — we iterated

Testing revealed users felt overwhelmed by legal copy on the sign-up page. Redesigned to lead with benefits, move legal disclosure below the fold. Completion rate improved measurably in the follow-up session.

"It was so much easier than I expected. I thought payments setup would be a nightmare."

— SMB Customer, Post-Launch Survey

"I can actually see when my money is coming. That alone makes it worth switching."

— SMB Customer, Post-Launch Survey

04b

The final sign-up page — rebuilt after testing

Testing (finding F4) showed the sign-up page overwhelmed users with legal copy. The final version strips it back to plain-language essentials with inline progress — the direct result of the usability sessions above.

05

Results — shipped on time, trusted from day one

Volume processed

$70M+

Transactions through the new system in the first quarter post-launch

Migration

70%

WePay customers migrated on time, meeting the 5-month deadline

Usability

73.9 SUS

Above industry average for payment products — rated "Good"

Payment volume

+30%

Volume increase post-launch vs previous processor — merchants were transacting more

Self-serve

95%

Users completed full setup without contacting support

Attach rate

+18%

Overall payment attach rate increase — more Keap users enabling payments than before

What I learned

Building a payments product as a sole designer taught me that constraints — hard deadlines, legal requirements, technical limitations — are not obstacles to good design. They're the conditions that make design decisions meaningful. Every simplification I made in the onboarding flow was a decision against something the legal or engineering team wanted to include. Making those tradeoffs visible and getting alignment on them was as much a part of my job as designing the screens.

The most important moment in the project wasn't any single screen — it was the design-studio workshop where we aligned cross-functionally on what "good" meant before writing a spec. Payment products fail when different parts of the organization have different success criteria. Getting product, engineering, payments, and design on the same page early is what made it possible to move fast without breaking trust with merchants.

What I'd do differently: I'd push harder for a payment health dashboard earlier — something that shows merchants not just their transactions, but trends, risks, and recommendations. The current dashboard is excellent for transaction visibility but passive. The next version should be proactive, alerting merchants before issues affect their cash flow.